Table of Contents

- Introduction: Why Fintech is Reshaping Careers

- Understanding the Shift: From Finance to Fintech Career Path

- Upskilling for Fintech Jobs: The Key to Success

- Fintech Certification for Working Professionals: Do You Need One?

- Fintech Training for Finance Graduates: What to Expect

- Emerging Fintech Job Opportunities in India

- Best Fintech Programs for Professionals to Consider

- Key Takeaways

- FAQs

- Conclusion

Introduction: Why Fintech is Reshaping Careers

The financial services sector shows constant change but its current speed of transformation reaches levels we have never seen before. Professional finance workers in India now see fintech careers as their main career direction instead of a specialized option. Technology now drives major changes in financial service delivery through mobile banking and blockchain systems which produces extensive new business possibilities. Traditional finance professionals who doubt their ability to enter fintech because they have spent years in the field should know that switching careers remains achievable. Your financial expertise becomes extremely valuable to the fintech revolution because this movement combines finance with technological solutions. This blog provides practical information for traditional professionals who want to enter the fintech industry through successful career transition.

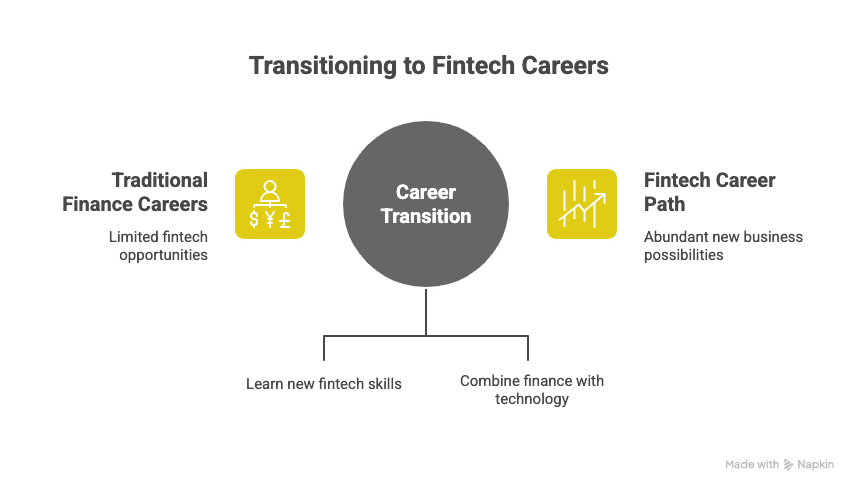

Understanding the Shift: From Finance to Fintech Career Path

The transition from finance to fintech requires professionals to develop digital competencies that enhance their existing core knowledge rather than abandoning their current specialization. All types of fintech companies including startups and established enterprises need employees who possess both financial fundamentals and the ability to operate within digital systems. The typical career shift from finance to fintech requires professionals to merge their understanding of financial markets and compliance with knowledge about emerging technologies including data analytics blockchain digital payments and AI. The table below offers a snapshot comparison between traditional finance roles and typical fintech roles:

| Traditional Finance Roles | Fintech Career Roles |

| Investment Banking Analyst | Blockchain Product Manager |

| Risk Analyst | Data Scientist – Fintech |

| Financial Advisor | Digital Wealth Manager |

| Compliance Officer | RegTech Compliance Specialist |

| Operations Manager | Fintech Operations Strategist |

The boundaries between finance and technology are fading, and professionals who can bridge that gap are in high demand.

Upskilling for Fintech Jobs: The Key to Success

The fast-moving nature of fintech demands more than just traditional finance qualifications to maintain market relevance and competitiveness. The ability to stay competitive in the job market requires non-negotiable upskilling for fintech positions. Multiple educational paths exist today to help you gain new skills through either brief online training or complete degree programs which concentrate on fintech. The skills you choose to develop for your career goals include coding and data analytics alongside blockchain and machine learning as well as product management. The following essential skills represent crucial areas for finance professionals to develop when they prepare for fintech positions.

- The tools -Python, SQL & Tableau serve as the essential components in data analytics.

- Blockchain & Cryptocurrencies: Understanding smart contracts & digital assets

- Artificial Intelligence and Machine Learning: Basic of automation & predictive modelling

- Digital Payment Systems: Knowledge of UPI, payment gateways, mobile wallets

- Regulatory Technology (RegTech): Automating compliance & risk management

- Cybersecurity Fundamentals: Securing financial data & digital transactions

External Resource: World Economic Forum – Future of Jobs in Financial Services

Fintech Certification for Working Professionals: Do You Need One?

The majority of finance professionals inquire about the requirement of official credentials to begin their fintech careers. A working professional certification focused on fintech provides substantial advantages for both professional recognition and job market opportunities. The process of obtaining certifications proves your dedication toward continuous education as well as your capability to follow emerging industrial developments. Through these programs you obtain organized educational content which would normally take several years of self-directed learning to achieve.

Some globally recognised and India-relevant certifications include:

- Imarticus Learning’s MBA in Fintech (Highly recommended for Indian professionals)

- CFTE’s Fintech Foundation Certification

- MIT Fintech: Future Commerce Program

- Oxford Fintech Programme

- Harvard’s Fintech Online Short Course

To explore a highly relevant option for Indian professionals, consider enrolling for the MBA in Fintech by Imarticus Learning—a comprehensive program that blends finance and technology, tailored for the Indian market.

Fintech Training for Finance Graduates: What to Expect

Newly graduated finance students along with beginning finance professionals frequently experience stress because of the fast technological advances in the industry. New finance graduates can succeed through fintech training programs that provide both technical abilities and business competencies. The training programs maintain modularity together with flexibility and they maintain alignment with current industry requirements. The courses span from basic financial system fundamentals to advanced blockchain development and digital lending platforms and data-driven financial product creation.

Here’s what typical fintech training for finance graduates covers:

- Fundamentals of Banking and Financial Markets

- Introduction to Financial Technologies

- Data Science and Analytics for Finance

- Blockchain and Cryptocurrencies Basics

- Digital Payment Ecosystems

- Fintech Product Development Lifecycle

- Regulatory and Compliance Landscape

External Resource: NASSCOM Report on Emerging Tech in Indian BFSI

Emerging Fintech Job Opportunities in India

The Indian financial technology industry experiences rapid growth because of increased digital usage and supportive regulations together with its tech-experienced population. The present moment represents the best time for anyone to join the fintech industry because of its multiple new fintech employment openings.

A report by EY predicts that India’s fintech industry will achieve $150 billion market size in 2025. The expanding market creates increased requirements for skilled workers who will fill various professional positions.

Here’s a look at some emerging fintech job opportunities:

- Product Manager – Digital Lending

- Data Scientist – Fintech Startups

- Blockchain Developer – Financial Services

- Cybersecurity Specialist – Digital Banking

- Payment Systems Architect

- Regulatory Compliance Analyst (RegTech)

- AI/ML Specialist for Financial Products

- Financial App UX/UI Designer

- WealthTech Financial Advisor

External Resource: EY India Fintech Report 2024

Best Fintech Programs for Professionals to Consider

The overwhelming number of programs available today makes it challenging to identify the best fintech programs for working professionals. The optimal program combines industry recognition with practical experience and technical skill development.

The selection of a program should prioritize these features:

- Practical case studies and real-world projects

- Industry partnerships and networking opportunities

- Mentorship from fintech experts

- Curriculum aligned with global fintech trends

- Flexible formats suitable for working professionals

Top recommendations for the best fintech programs for professionals include:

- MBA in Fintech – Imarticus Learning (India-focused and industry-driven)

- CFTE Fintech Foundation Program

- MIT Fintech: Future Commerce Course

- Oxford Saïd Business School Fintech Programme

- Harvard Fintech Online Short Course

These programs can significantly accelerate your transition to a career in fintech, providing both credibility and in-demand skills.

Key Takeaways

- The demand for professionals with both finance and tech skills is soaring in India.

- A career in fintech allows finance professionals to future-proof their careers.

- Upskilling for fintech jobs is essential, with focus areas like data, AI, and blockchain.

- Pursuing a fintech certification for working professionals enhances credibility.

- Fintech training for finance graduates equips young professionals for industry demands.

- India’s emerging fintech job opportunities cover roles in AI, blockchain, cybersecurity, and more.

- Choosing from the best fintech programs for professionals can fast-track your career transition.

FAQs

1. Is it hard to switch from finance to fintech?

Fintech transition becomes accessible when you stay willing to acquire fresh technical knowledge. Your finance experience helps you establish a foothold yet you need to add appropriate technology competencies.

2. What skills do I need for a career in fintech?

To remain competitive in fintech you need to acquire skills in data analytics and blockchain together with AI/ML and digital payments and cybersecurity on top of your finance expertise.

3. How long does fintech training for finance graduates typically take?

Fintech training duration varies between programs because short courses run for 3 to 6 months but an MBA in Fintech requires 12 to 18 months to complete.

4. Are fintech certifications recognised by employers?

Employers in the fintech industry highly regard certifications obtained from Imarticus as well as MIT and Harvard institutions.

5. Can non-tech professionals build a fintech career?

Absolutely! Many fintech roles such as -product management, operations & compliance, do not require deep technical expertise but do need understanding of technology’s impact.

6. What are the salary prospects in a fintech career?

Salaries vary based on role and experience.. but fintech often offers higher growth potential compared to traditional finance, especially for specialised roles like blockchain development or AI in finance.

7. Is India a good market for fintech jobs?

Yes.. India’s fintech market is booming -offering vast job opportunities due to high digital adoption, supportive government policies, and a large unbanked population.

8. Do I need to know coding for fintech jobs?

Not always. While technical roles may require coding, many non-tech roles in fintech value business, finance, and regulatory knowledge.

9. Which industries within fintech are growing fastest?

Digital lending, payment solutions, wealth tech, blockchain & RegTech are among the fast growing fintech segments in India.

10. How do I start exploring fintech career options?

Begin by researching roles that align with your interests – enrol in fintech training or certification programs & build your network within the fintech ecosystem.

Conclusion

Let’s be real: fintech isn’t just a buzzword anymore—it’s the center of gravity for anyone serious about a future in finance. The game’s changed. If you want to stand out, you’ll need to – keep upgrading your skills, collect the right certifications & actually get involved in the industry.. not just watch from the sidelines. Doesn’t really matter if you’re just starting out or you’ve been around the block—a proactive approach opens a lot of doors.

If you’re genuinely eyeing this shift, the MBA in Fintech by Imarticus Learning is worth a look. The program’s designed to build your expertise, expand your network (yeah, connections still rule), and give you the confidence to compete—and win—in fintech’s fast-moving world.

The future of finance is digital. The question is—are you ready to be part of it?