Last updated on June 3rd, 2025 at 11:23 am

Last Updated on 10 months ago by Imarticus Learning

If you’re trading options or preparing for a financial risk exam, you’ve probably asked yourself this: How exactly is an option priced? You see prices on the screen calls, puts, and strikes, but behind those numbers is a world of maths, probability, and assumptions.

Understanding option valuation isn’t just for quants or traders. It’s essential for analysts, finance students, and anyone serious about risk management. Whether you’re tackling the FRM exam or analysing derivatives in your job, you need to know models like the Black-Scholes model. But here’s the catch: these models aren’t perfect. That’s where other option pricing models come in.

What Is Option Valuation, and Why It Matters

Option valuation is the process of calculating what an option is really worth and its fair price based on key factors like the price of the underlying asset, strike price, time to maturity, interest rates, and volatility.

It matters because:

- Without knowing an option’s value, you’re trading blindly.

- Overpaying means losses.

- Undervaluing means missed profit.

Whether you’re in trading, compliance, or a financial risk management course, understanding option valuation helps you manage exposure, hedge properly, and make better decisions.

Core Inputs for Option Valuation: The Five Key Ingredients

Every pricing model depends on a few standard inputs:

- S = Current price of the underlying asset

- K = Strike price of the option

- T = time to expiration (in years)

- r = Risk-free interest rate

- σ (sigma) = volatility of the underlying asset

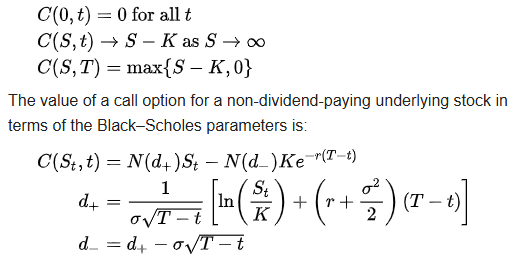

The Black-Scholes Model

Together, these decide the premium you’ll pay (or receive) for an option. Whether you use Black-Scholes or another option pricing model, these remain constant.

Developed in 1973, the Black-Scholes model revolutionised modern finance. It assumes markets are efficient, prices move in a lognormal way, and you can continuously hedge a position.

The Black-Scholes formula is basically used to work out the price of European call and put options. It ties directly back to the Black-Scholes equation, which it solves under specific final and boundary conditions. The formula gives you the option’s value based on maths that models how prices behave over time.

The core formula for a call option:

Even if this seems too mathematical, here’s what you should remember: the model calculates the probability-weighted value of the potential future price movements.

Comparing Option Pricing Models

| Feature | Black-Scholes | Binomial Model | Monte Carlo Simulation |

|---|---|---|---|

| Time Frame | Continuous | Discrete | Random Simulations |

| Volatility Assumption | Constant | Variable (can adjust) | Flexible |

| Complexity | Low | Medium | High |

| Useful For | European Options | American Options | Exotic or path-dependent |

| Speed | Fast | Slower | Slowest (needs iterations) |

The Black-Scholes (B&S) model has long been the go-to framework for pricing options. It offers a clear and structured approach built on solid mathematical foundations.

While the Black-Scholes model is great for quick estimates, many prefer binomial or Monte Carlo methods for real-world flexibility. This is especially useful in financial risk management courses where scenario-based learning is common.

What Black-Scholes Gets Wrong (and What’s Beyond It)

Let’s be real: the Black-Scholes model works best under textbook conditions. But markets are messy. Volatility isn’t constant. Interest rates change. And guess what? You can’t hedge every second.

That’s why other models emerged:

- Binomial Tree Model: Breaks the time frame into steps, allowing different outcomes at each point.

- Monte Carlo Simulation: Runs thousands of random price paths to see how an option performs.

- Stochastic Volatility Models (like Heston): Allow volatility to change with time.

In real life and in any solid option valuation curriculum, you’ll learn when to use which.

Why do option pricing models matter in risk work?

- They help value structured products.

- Support decisions on hedging large positions.

- Feed into broader value-at-risk (VaR) models.

Any serious financial risk management course spends a good amount of time here. You’re not just memorising formulas, you’re applying them to limit losses.

Common Mistakes You Can Avoid

The Black-Scholes model, also called the Black-Scholes-Merton model, was the first option pricing model to gain widespread use. It helps calculate the value of European-style call options using known inputs like the stock’s current price, the option’s strike price, and time to maturity, all based on certain assumptions about how asset prices behave.

It works by taking the stock price, adjusting it with probability factors, and then subtracting the discounted value of the strike price, again adjusted for probability. This gives you a fair estimate of what the option should be worth today.

- Blindly trusting Black-Scholes: Remember its assumptions.

- Ignoring volatility changes: Markets swing, your model should reflect that.

- Forgetting transaction costs: These affect hedging accuracy.

- Applying European formulas to American options: Rookie mistake.

Every option valuation mistake costs money or marks on your exam. Avoiding them is half the battle.

Build a Career in Risk Management with Imarticus Learning FRM Certification

The FRM Certification at Imarticus Learning is for finance professionals who want to master risk and build a global career. With access to over 300 hours of expert-led training, 4000+ practice questions, and personalised mentorship, this course helps you gain practical skills and theoretical clarity.

You also get Analyst Prep, the top-rated GARP-approved platform to study efficiently. And if you don’t pass the FRM exam, you get your money back. That’s the pass guarantee. Alongside this, you’ll get prepared with resume reviews, interview guidance, and career bootcamps to make you job-ready.

Whether you’re eyeing roles in risk, investment, or compliance, the Financial Risk Manager (FRM) Certification at Imarticus Learning gives you an edge.

Start learning with full confidence today.

Enrol now in the FRM Certification by Imarticus Learning.

FAQ

Q1. What is option valuation in finance?

Option valuation is the method used to find a fair price for options based on factors like volatility, interest rates, and time to expiry.

Q2. Is the Black-Scholes model outdated?

It’s still widely used, but for real-world scenarios with changing volatility, other option pricing models offer more accuracy.

Q3. Which model is best for learning in a financial risk management course?

The Black-Scholes model is often the starting point, followed by binomial and Monte Carlo methods in FRM and CFA programmes.

Q4. Why do option pricing models matter in risk management?

They help assess and control financial risk, making them essential for portfolio managers and FRM-certified professionals.

Q5. Do these models apply to American options?

Black-Scholes is for European options. For American options, use binomial trees or finite difference models.

Q6. How do I practice option valuation?

Join a financial risk management course or use simulation platforms that let you work with real datasets and scenarios.Q7. What is the best course for learning option pricing models in India?

The Financial Risk Manager (FRM) Certification from Imarticus Learning is a top option with practical training and global recognition.