Last Updated on 7 months ago by Imarticus Learning

All small and large firms prepare budgets to estimate revenues, expenses, and profits. Financial outcomes always never so exactly occur as budgeted. That is where variance analysis comes in between actual and budget.

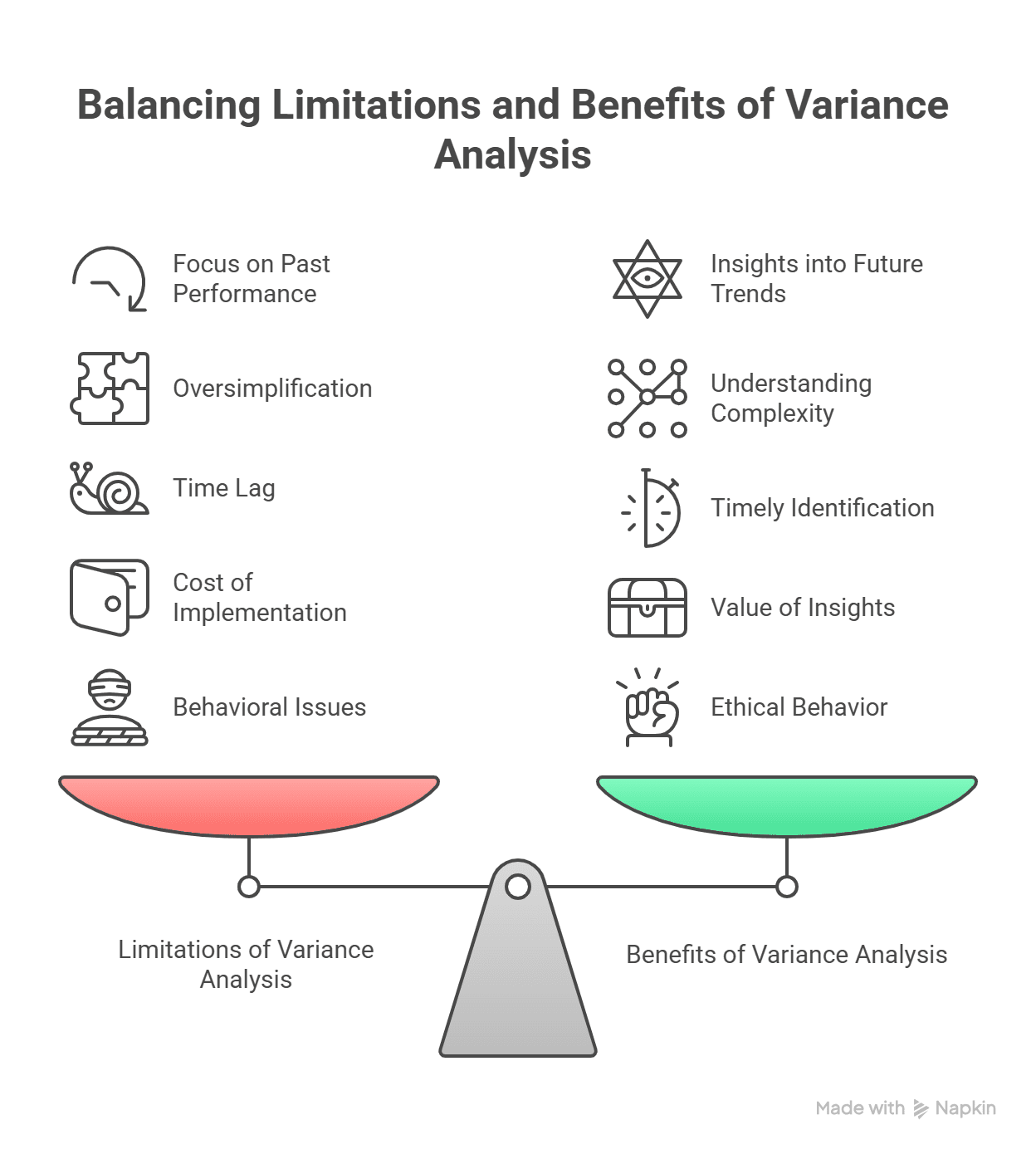

Variance analysis is one of the scientific methods of discovery that discover, investigate, and analyze financial variances between what has been forecasted and what happens. Budget variance analysis enables companies to determine areas of wastefulness, constrain costs within thresholds, and make intelligent fiscal decisions.

In this blog, we will be covering the topic of the day—budget variance, cost variance, favorable and unfavorable variance. We will also understand why finance professionals must become a variance analysis guru, and how educational programs like the Postgraduate Financial Analysis Program can make you one.

What is Variance Analysis?

Variance analysis is the process of comparing amounts of money incurred with budget or standard amounts with the purpose of knowing the difference and why. The variances will be favorable (positive) or unfavorable (negative).

Explanation:

Actual revenue is greater than the budgeted revenue, so it’s a favorable variance.

Actual expenses are greater than what was budgeted, so it’s an unfavorable variance.

Variances analysis help finance departments to compare performance, plan for future improvements, and better-informed decision-making.

Importance of Variance Analysis in Budgeting

Why is variance analysis for budgeting so crucial? Let us enumerate the key reasons:

Performance Measurement – It shows where departments or teams have been relative to goals.

- Cost Control – Shows where costs have been overspent.

- Accuracy of Forecasts – Refines future budgets based on lessons from past errors.

- Decision-Support – Suggests to the management to re-prioritize and re-allocate resources effectively.

- Accountability – Refers departments accountable in being on track to organizational goals.

Brief, budgets would be theoretical journals and not of practical usage if they did not provide variance analysis.

Types of Budget Variances

There are several types a budget variance can be. The following are the most general categories:

1. Revenue Variance

It is when the actual revenue and budgeted revenue do not align. It may be due to various prices, quantities sold, or demand levels.

2. Cost Variance

It is different from the actual cost and budget cost. Cost variance is usually classified as:

- Material Variance – Raw material prices above or below what was anticipated.

- Labor Variance – Labor cost at different levels from planned levels.

- Overhead Variance – Variation in utilities, rent, or other fixed cost consumption.

3. Profit Variance

Any time net income varies from what was expected by a change in revenue and expenses.

4. Cash Flow Variance

Budgeted versus actual inflows/outflows of cash with a very immediate impact on liquidity.

These budget variances provide a basis for taking proper action and performance measurement.

Actual vs Budget: Why the Difference Matters

Budget vs. actual comparison is an important component of management reporting. It tells the stakeholders what extent of deviation the business had from its budget.

Example:

- It was budgeted for sale of ₹10,00,000 but achieved ₹12,00,000. The variance is +₹2,00,000 (favorable or positive).

- If it had budgeted to spend ₹5,00,000 but spent ₹6,00,000, the variance is -₹1,00,000 (unfavorable or negative).

Recognising these differences enables leaders to shift gears—through budget maneuvering, lean efficiency, or new strategy targeting.

Cost Variance: A Closer Look

Of all variance measures, cost variance is the most significant. Because expenses have a direct influence on profitability, monitoring cost variance meticulously is crucial.

Common causes of cost variance include:

- Supplier’s volatile prices.

- Labor cost or overtime when they are not anticipated.

- Ineffective production procedures.

- Rising utility or overhead rates.

To the accountant, variance analysis of costs is not simply messing with budgets but it is also an alert for underlying supply chain and operations issues.

Favorable vs Unfavorable Variance

That is not necessarily all bad while performing variance analysis.

- Favorable Variance – When actuals are higher than expected. Example: lower cost or greater revenue.

- Unfavorable Variance – When actuals are worse than expected. Example: increased expenditure or decreased sales.

Favorable vs unfavorable variance keeps managers from merely responding to numbers but responding to them the way they should. Favorable variance literally, in certain instances, even represents under-utilization of resources, while an unfavorable variance can represent investment needed.

How Variance Analysis Improves Business Decisions

Budgeting variance analysis is not figures—it’s decision. It helps companies:

- Spotting poorly performing areas.

- Improving marketing or pricing strategy.

- Negotiating better terms with the supplier.

- Putting money into more profitable investments.

- Holding individuals accountable.

- Employees being held accountable.

In reality, variance analysis enhances short-term performance and long-range planning.

Variance Analysis in Finance Careers

Financial professionals, especially analysts, FP&A professionals, and accountants need to be variance analysis wizards. Recruitment companies hire individuals who do not just run variances, but also tick why they happen and suggest what needs to be done to rectify them.

It is from here that courses like the Postgraduate Financial Analysis Programme are required.

Postgraduate Financial Analysis Program: Your Path to Expertise

Imarticus Learning’s Postgraduate Financial Analysis Program will nurture expertise in financial analysis—like careful budgeting and variance analysis.

Program Highlights:

- 100% Job Guarantee with 7 sure-shot interviews.

- 56,000+ placements with 500+ hiring partners.

- 60% average salary boost for learners.

- Flexible Learning: 4-month weekday or 8-month weekend options.

- Recognition: Awarded Best Education Provider in Finance at the 30th Elets World Education Summit 2024.

Skills You’ll Gain:

- Financial statement analysis.

- Variance analysis and financial modeling.

- Equity research and valuation.

- Transaction execution and corporate finance insights.

- Excel and PowerPoint skill sets.

Learning Approach:

- Practice simulation tools.

- In-class activities and real-life case studies.

- Personal branding and LinkedIn assignments for professional growth.

With careers like FP&A Analyst, Equity Research Analyst, or Treasury Analyst in the pipeline, this program accelerates your career path.

Gather in-depth knowledge about a plethora of concepts between trading and financial modeling in this video- Trading to Financial Modeling Pro: Ramit’s PGFAP Story | Postgraduate Financial Analysis Program

Real-life Example of Variance Analysis

Let us take an example:

Company’s sales budget was ₹50,00,000 and expense budget was ₹30,00,000. Actual sales were ₹48,00,000 and actual expenses were ₹32,00,000.

- Sales Variance = -₹2,00,000 (adverse).

- Expense Variance = -₹2,00,000 (adverse).

- Profit Variance = -₹4,00,000 (adverse).

This means that the management will have to work again on sales strategy and cut wasteful expense.

FAQs

Q1. What is variance analysis?

Analysis of variance is a technique to compare actual and budgeted amount of money for the sake of knowing and distinguishing differences.

Q2. What is budget variance?

A favorable or unfavorable difference between actual and budgeted figures.

Q3. What effect are cost variances having on companies?

Cost variance informs companies how much they are spending less or more on material, labor, and overhead and makes them ask themselves how they can save money.

Q4. Describe favorable vs unfavorable variance.

Positive variance is the experience of better-than-expected performances, and negative variance is experiencing slowdowns.

Q5. Why is variance analysis so important in budgeting?

It helps with tracking of performances, cost reduction, better forecasting, and better financial decision-making.

Q6. Is variance analysis employed outside of finance?

Some locations employ it in project management, operations, and even human resources for performance monitoring.

Q7. How do businesses deal with negative variances?

By savings that are created by cost reduction, contract negotiation, added efficiency, or budget adjustment.

Q8. What packages are used in variance analysis?

Excel, BI software, and accounting packages are primarily used.

Q9. Is variance analysis useful to individuals?

Yes, individuals can use it for their own cost control and budgeting.

Q10. How effective is the Postgraduate Financial Analysis Program?

It instills career-focused financial skills like variance analysis, modeling, and career placement.

Conclusion

Variance analysis is not activity accounting—any rational management tool that leads to better business performance. With budget variance, cost variance, and favorable/unfavorable variance information, business organizations have the data needed to manage resources better.

For accountants, variance analysis is not a matter of choice. With greater demand for capable analysts, formal learning like the Postgraduate Financial Analysis Program can be a career-advancing asset.

So the next time you were testable on variance analysis, you’ll find there’s more to variance analysis than numbers—there is better financial decision-making at stake.