The expense of the CFA program is a serious consideration factor among students and financial professionals making this highly coveted professional designation decision. Aggregating fees for exams, study guide expenses, and coaching expenditures, it is only logical to establish the total cost of the CFA program prior to admission.

Is it justified to invest in the CFA course? It would depend on a sequence of variables like career growth, pay raises, and overseas job opportunities.

Chartered Financial Analyst (CFA) is one of the most valued finance certifications. With a typical pay raise of up to 192%, CFA charterholders typically enjoy good-paying jobs in investment banking, portfolio management, and risk assessment.

This CFA course fee structure guide gives you a systematic comparison so that you can compare and contrast registration fees, study material fees, and other investments and take an informed decision.

CFA Course Price: A Complete Breakdown

The total cost of the CFA course is an aggregate sum of the following factors:

- Exam Fees (Registration Fee & Enrollment Charge)

- Study Material & Prep Course Fees

- Other Fees (Reschedule, Retake, Membership Fees)

Total cost for the whole CFA certification (Level 1, Level 2, and Level 3) ranges from $3,000 to $4,500 (₹2.5 lakh to ₹4 lakh) on average.

Let’s analyze each item of the costs separately.

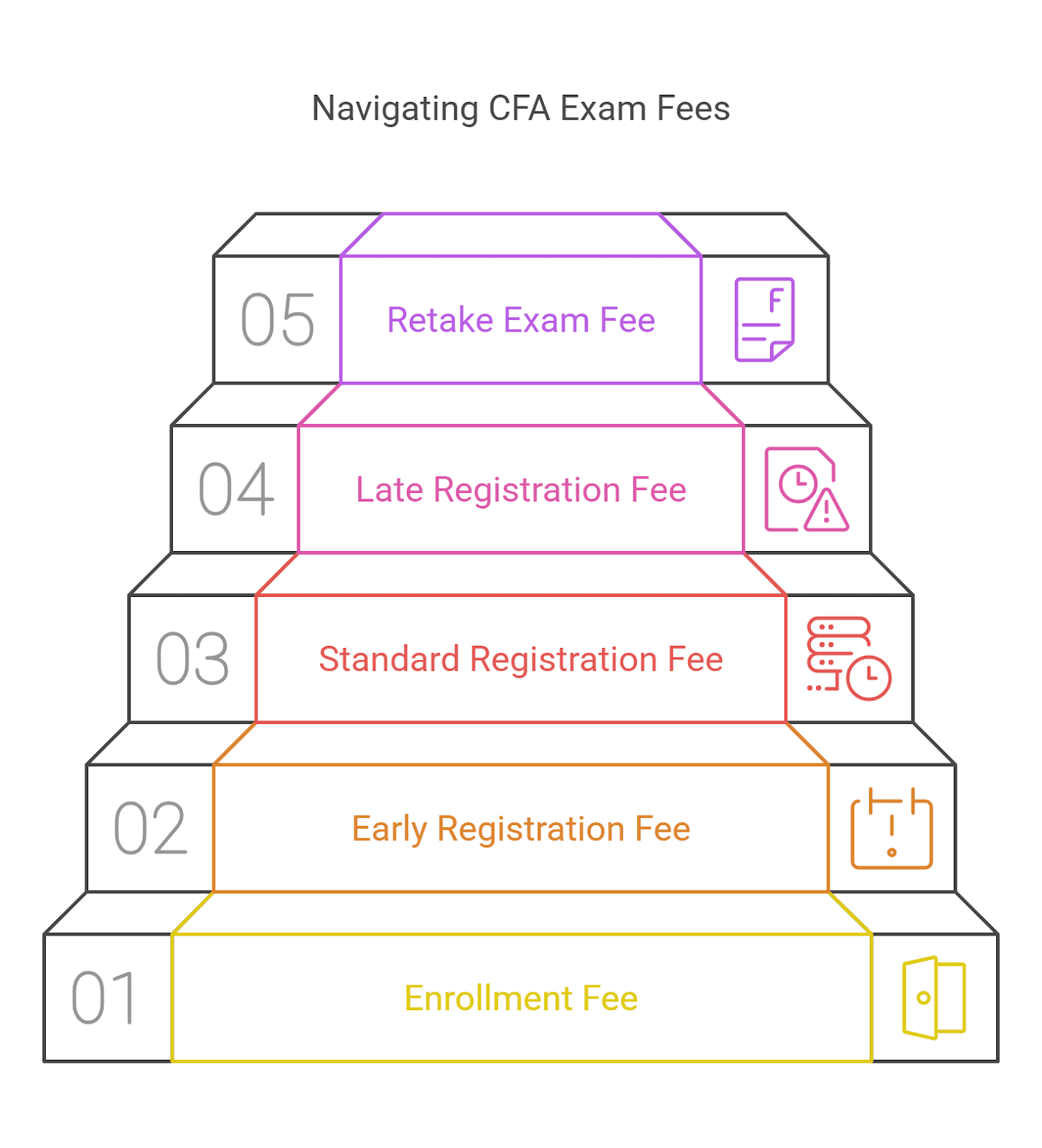

1. CFA Program Fees: Exam Registration & Enrollment

The CFA certification is of three levels, and the candidates have to pay various exam fees for each level. Below is a detailed CFA course fee structure:

| Fee Type | Cost (USD) | Cost (INR Approx.) |

| One-time Enrollment Fee (for Level 1) | $350 | ₹29,000 |

| Early Registration Fee (Per Level) | $940 | ₹78,000 |

| Standard Registration Fee (Per Level) | $1,250 | ₹1,04,000 |

| Late Registration Fee (Per Level) | $1,450 | ₹1,20,000 |

| Retake Exam Fee (Per Level) | Same as Standard Fees | ₹1,04,000 |

Key Takeaways:

✔ Early registration saves up to $300 per level – Best for cost-conscious candidates.

✔ Level 1 one-time $350.

✔ Full fee retakes – No waiver on failure.

2. CFA Study Materials: Self-Study vs. Paid Courses

CFA Study Material Choices:

| Study Material | Cost (USD) | Cost (INR Approx.) |

| CFA Institute Curriculum (Official) | Included in Registration Fee | ₹0 |

| Kaplan Schweser Study Packages | $400 – $1,200 | ₹33,000 – ₹99,000 |

| Wiley CFA Study Materials | $600 – $1,500 | ₹50,000 – ₹1,25,000 |

| Bloomberg CFA Prep | $1,000 – $2,500 | ₹83,000 – ₹2,07,000 |

Which CFA Study Option is Best?

- Self-Study: Best for independent candidates with limited budget.

- Paid CFA Courses: Best fit for those candidates who need a structured learning process and guidance.

Kaplan Schweser is the one that most of the CFA candidates go for because it is the full package from video lectures, question banks, to practice exams.

3. Additional CFA Course Investment: Hidden Costs

Buried Costs in CFA Course Investment:

| Additional Cost | Estimated Cost (USD) | Estimated Cost (INR) |

| CFA Exam Rescheduling Fee | $250 | ₹20,500 |

| CFA Membership Fee | $275 per year | ₹22,000 per year |

| Exam Resit/Retake Fee | Same as Exam Fee | ₹1,04,000 per level |

| Travel & Accommodation (For Exam) | $200 – $500 | ₹16,500 – ₹41,500 |

CFA Course Price vs. ROI: Is It Worth the Investment?

Now that the CFA course fee structure is out, let’s calculate if the investment is worth the price by considering probable salary increases, job opportunities, and industry demand.

1. Salary Growth After CFA Certification

Salary comparison before-and-after CFA certification:

| Job Role | Without CFA (INR) | With CFA (INR) | Growth % |

| Financial Analyst | ₹6 LPA | ₹12 LPA | +100% |

| Investment Banker | ₹12 LPA | ₹25 LPA | +108% |

| Portfolio Manager | ₹10 LPA | ₹30 LPA | +200% |

| Risk Manager | ₹9 LPA | ₹22 LPA | +144% |

Average salary hike after CFA: Up to 192%.

FAQs on CFA Course Price & Investment

1. India fee for entire CFA course?

India fee of full CFA certification (all levels) without exam fee, study guides, and prep courses is ₹2.5 lakh to ₹4 lakh.

2. Is CFA exam fee refundable?

No, CFA exam fees are not refundable. If you don’t attend an exam, you must pay again to register.

3. Is there a CFA fee installment facility?

Yes, there is an EMI facility for coaching and studies from most of the CFA prep providers. CFA Institute does not have installment plans, however.

4. Is CFA cheaper than an MBA in Finance?

Yes, the cost of the CFA course is much cheaper compared to an MBA in Finance. MBA is ₹20-50 lakh and CFA is ₹2.5-4 lakh only.

5. Is financial aid available to pursue the CFA course?

Yes, financial aid in terms of scholarships by CFA Institute waives fees up to 85% for meritorious students.

6. Does CFA assure a high salary?

While CFA aids career development, salary increments are based on experience, rank, and location.

7. Are paid study courses for CFA worth the cost?

Yes, paid classes increase pass rates over two times with organized tutoring, practice examinations, and expert advice.

8. How do you reduce CFA exam cost?

Save by early registration, scholarship application, and first-time pass to reduce overall cost.

Conclusion: Should You Invest in the CFA Course?

The price of the CFA course is high, but return on investment is assured. With a potential return on investment of up to 192% in salary growth, global career opportunity, and prestige, CFA is one of the finest investments for finance professionals.

If you’re hell-bent on pursuing a well-paying finance job, CFA certification is each dollar’s worth.

What’s Next?

Join a CFA study course today

Save dollars by registering in advance

Take the first step to CFA success